In my continuing exploration of the deepest P/B decile i have perhaps found another bargain.

From google finance: “Cathedral Energy Services Ltd is a Canada-based company, which is engaged in the business of providing selected oilfield services to oil and natural gas exploration and development entities in western Canada and the United States. The Company carries on its activities in Canada and the United States under the name Cathedral Energy Services with operating division Directional Drilling. The Directional Drilling division provides horizontal, directional and underbalanced drilling services. The Directional Drilling division has approximately 60 Measurement While Drilling (MWD) systems in Canada and over 80 in the United States.”

Management owns approx 6% of the outstanding shares and 40% is owned by Franklin Resources which perhaps is not optimal due to its big size. The company have in the last year reduced its debt down to zero through sale of assets but also by issuance of new shares.

Also, the share issue this year is the first on at least 10 years (without taking consideration of management options).

Unfortunately the company have heavy leasing obligations on 35M CAD. It mostly refers to buildings.

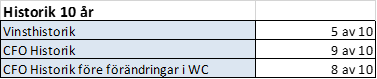

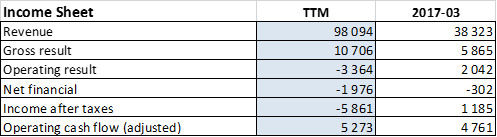

The company has mentioned that the outlook looks much better this year than the year before and the first quarter have delivered positive returns and operating cash flow. Even though EV/OCF don't look great it is actually mostly the last quarter that contributes to it.

I’m having trouble to understand why they needed cash so much that they would issue shares. They have had some trouble the last couple of years and perhaps some trouble with the banks. I'm not certain that it was a last resort solution which makes me more reluctant, but on the other hand the money did not go to a bad cause like financing salaries for the management, but to reducing debt to zero. And it did happen in the worst year of the company history.

Now the financial situation looks a lot better. Unfortunately there is still the leasing obligations that makes the financial position a little bit unfair.

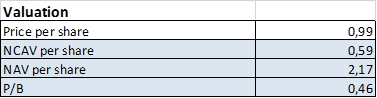

The stock trades a lot higher from its all time low 0,3 CAD in the last spring compared to today's 1 CAD, but the situation has also changed alot since then. The financing issue is solved, cash flow is positive and the outlook looks good.

In this range of P/B companies everything will not be perfect. You can't have it all. My thesis is that the risk of losing money on this investment is low and that the upside is bigger than the downside. With the new financial situtation i don't expect that it will be necessary with any more capital injections the coming year. With once again positive cash flows as a trigger and no outstanding debt i think this stock looks like a bargain. Bare in mind that i hold my positions only one year and that’s how far i “predict”.

What do you think about this case?

I am long Cathedral Energy Services